9 Basic Budgeting Tips for Beginners

There is no need to cringe when hear the word “Budget”. Deciding to start and continuing to maintain a budget on a consistent basis can not only give you insight on where and what your money is being spent on, it can also help you stay far away from making bad debt decisions.

By adhering to some basic budgeting tips, you can always know how much money is coming in, know how much money is going out and create a sense of financial freedom for you and your family.

So, whether you’re just starting out and are thinking about creating a budget or your deep in the game and already have a detailed budget lined out, these 10 basic budgeting tips can be used to give you helpful information to either start out on the right foot are continue to maintain a healthy, viable budgeting machine!

1. SET GOALS

What do you want your money to accomplish for you? For my wife and I, our main reason for starting a budget was to find out where in the world our money was going!

There were too many months were we looked at our bank account and just couldn’t understand why what was going out was “higher” than what was coming in. Come to find out, we were hitting up fast food restaurants and going to the grocery store to pick up snacks and junk food like crazy.

After starting a budget, we began to track the items that we were spending money on and also put them into categories to get an idea on where our money was going.

We also looked “back” a few months to further grasp where our money was going and it, to say the least, was an eye opener.

After we found out where our money was going, we were able to put together a plan of attack to correct the problem. Within two to three weeks, not only were we able to track how much we were spending on average, we were able to tailor a budget that would keep us within a reasonable spending amount for groceries, eating out, items for home and more.

So identifying a goal for your budget is key part of setting yourself up for success. Keep in mind that you may not hit your budgeting goals at first but through persistence and hard work you can definitely make progress. Plus, like my goals currently, they may alter and change as well.

Sign Up for our Newsletter to get Helpful Tips on Making and Saving money.

2. BE REALISTIC

When you’re starting out, and budgeting is a brand new concept to you, this is the time when you definitely have to be realistic about your budget.

Believing that you are going to cut everything down to a bare minimum (and some do, I did and we soon had to adjust) and make it work may do more harm than help.

Some may feel as if they are giving up “too” much to make everything work and soon give up and quit completely.

Although in some extreme cases, this may seem like your only option, most times there are ways to make a reasonable budget by calculating your income and forecasting how much is going out per month to get an idea on how much you will be spending.

3. CALCULATE YOUR INCOME

Calculating your income is a very important step. Make sure to gather “all” sources of your income.

This may include your salary that you earn at work, alimony, rental income, child support and any other source that you have coming in.

Also make sure to set up your budget based on your Gross income. This is the amount of money that you “take home” at the end of the day.

Power Tip:

– If you have a yearly salary and you want to calculate your monthly income, just take your yearly salary and divided it by 12 for 12 months in the year.

Salary / 12

– If you get paid the same amount every week, multiply your weekly pay by 52 and divide the total by 12.

Weekly Pay * 52 / 12

– If you get paid the same every two weeks, multiply your weekly by by 26 and divide the total by 12

Bi-weekly pay * 26 / 12

4. GATHER YOUR EXPENSES

Not only is it important to budget for expected expenses, it is important to budget for unexpected expenses. Lance, what do you mean by that.

Well, I own a house and we still use a home warranty, partly because my furnace is on its last legs. My wife and I are looking to replace it next year, but until then, anything can happen. And in the last 2 years, that anything “has” happened. Literally.

Every time a Heating & A/C technician had to come out to our home, they charged us $100, but the amount of service that they have fixed and taken care of for us has “far” outweighed the amount that we have paid for the warranty itself and they yearly warranty fee.

So keep aware of things that are unseen at the time especially if you own a car, home or have kids. Don’t get me started talking about unexpected children expenses. Sheesh.

Also, make sure to avoid unnecessary expenses that you don’t use or have a use for like gym memberships (especially if you don’t go on a consistent basis).

Instead, maybe you can borrow some fitness tapes from the library, run outside or save up for an inexpensive bowflex or treadmill for your home.

Cutting the unnecessary expenses (and you know what they are) can help you free up more money to pay off bills quicker, have more money set back for when those unexpected expenses come up, or to build up your savings account.

5. GET ORGANIZED

There has to be some type of system that you have in place to stay on track and keep organized. Keep Good, accurate record keeping and operate on a regularly routine to stay up to date with your income and expense entries.

Below I’ll cover more about using software or spreadsheets to keep on track but it is imperative that you use something that is going to keep your budget cataloged in a systematic way so that at a glance you can see how you are doing at any given time of the month.

They more organized you are, the more you can tweak your budget for an adjustment and make smart decisions about how you manage your money.

At the time of this article, I manually input my income and expense entries into a budgeting spreadsheet every day/week. I know, drudgery right?

I’ll eventually switch at some time to a more modern way of keeping track of my money, but at this time, I want to make sure that I evaluate every single transaction that goes in and out of my account and I want to go through the painstaking process of manually inputting every entry.

This keeps me accountable and forces me to come face to face with every transaction and unnecessary gadget that I buy from time to time.

6. SETUP SOME TRACKING METHOD

As I said earlier, you need to have some sort of way that you are going to track your income and expenses, even if you write down everything in a notebook and keep it logged.

Now, to me, writing you budget down on a notebook is not very advantageous, it would be so much better if you were to look into using a spreadsheet that you can save on google docs to access anywhere or use a number of the popular budgeting software programs on the market to suit your needs.

By using a spreadsheet to track your expenses, you can see calculations of your percentage saved per month, the amount of money you have left to spend in your defined expense categories and record how much income can go towards a number of your bills that need to be paid on a regular basis.

They same goes for most budgeting software. Most software can also be connected to your banking and investment accounts and automatically track your income and expenses in real time. It does the work for you.

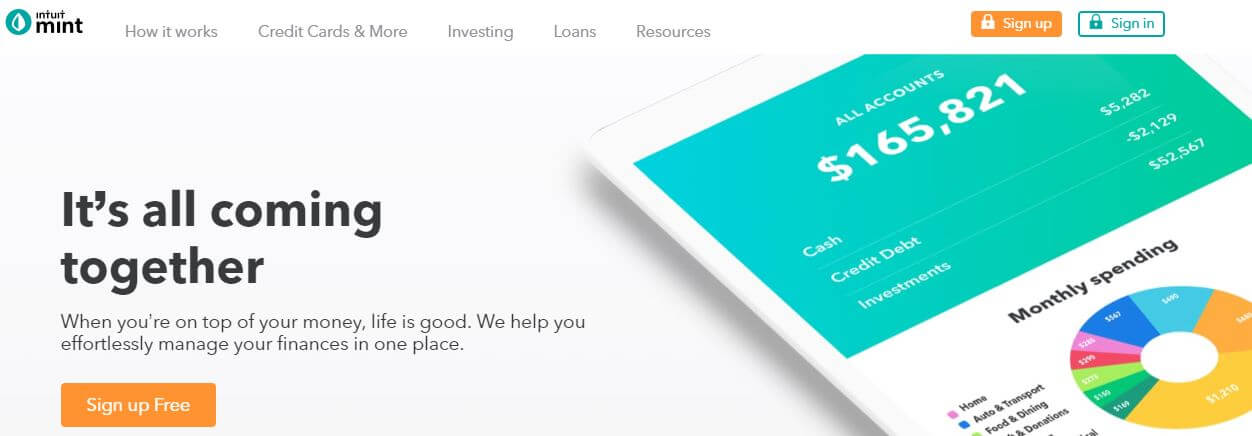

One example is a software called Mint which is developed by the good folks at Intuit. I actually use mint because it is free but the interface, to me, is kind of clunky and it takes a little bit of time to navigate.

One other thing that I don’t like is that you can not assign or create your own categories; you have to use the predefined ones that they have created.

But, nevertheless, it is free and someday I may master it and use it instead of my trusty spreadsheets to organize my expenses.

7. STOP IT WITH THE EXCUSES

I’ve heard it all:

“I don’t know where to start.”

“I might mess it up.”

“I don’t need one.”

“I don’t like numbers”

And on and on and on………

In the words of Mr. Wonderful: STOP THE MADNESS!

In most cases, it simply boils down to just doing it. You can use a simple budgeting spreadsheet to update your income and expenses and it will do the calculations for you.

If you would like a more automated method there are several free and paid options that connect to your bank account, categorize and manage your expense and income and then give you snap shots of key areas that you are doing well in and areas that may need attention.

And if you believe that you don’t have the discipline or may not be consistent over time; that’s ok.

Creating and having the willpower to keep up to date with expense entries, or reducing your spending for a specific time in a specific area may seem like a battle, but what you are working towards will far outweigh the headache.

If you are in debt then a budget can help curb your spending habits, make you aware of your current financial state and give you an outline on how to improve your situation.

Even if you’re debt free, having a budget can keep you on track for retirement or while you’re actively in your retirement years.

8. THERE CAN BE, NO, THERE WILL BE DISAPPOINTMENTS

You can “plan” all you want, but something will always rise up to be the unexpected thorn in your flesh.

You’re not always going to hit your goals. Unexpected events come up in our lives all the time, especially if you have a house. The second year of owning my first home, we had a huge wind storm and ton shingles blew off of my roof.

We had the insurance company come out and a representative came out to get an assessment of the damage. He told us that they damage was on the border line of getting a full payout, but we had a pretty good shot. Much to our surprise, our insurance company paid the entire cost to get our roof replaced!

Now, we had to pay a $1000 deductible out of pocket and I ended up paying a lot more because I wanted some of the most durable shingles and some other wind guards, but in the end we ended up paying around $2,200 out of pocket.

Now $2000 is not that easy to come by and later on that year we had some furnace problems, and also welcomed our first child, so our budget was all over the place.

Occasionally, you may encounter some huge changes in your budget……and it’s ok. This typically is not the norm; at least it shouldn’t be.

Having to have to adjust your figures and recalculate goals due to financial ups and downs can be disappointing, but it is nothing that you can not recover from with time.

9. MOTIVATION & INVOLVEMENT

Whenever you get down or discouraged about any low points in your financial journey, just try to focus on the big picture: getting and/or staying out of debt. Some ways that you can keep motivated is to:

- Involve friends and family in your mission. Discuss your goals and ambitions and have them keep you accountable.

- Reward yourself from time to time. If you can afford to, and if you’re not in debt to the point where it’s either go to the movies to hang out with friends or pay the light bill……..then treat yo’ self

- Use goal reminders and visual media. Stick up goal charts to color in if you’re paying off a certain debt, put up pictures of your kids or a house that you want to purchase, hang up motivational quotes or sayings to keep you going. Do what you have to do to keep yourself focused.

- Keep out of the Trap. My trap is stores like Dollar Tree. I’ll go inside, intending to get “one” item and I end up coming out of the store with an easy reach pick up tool, a pack of lemon heads, a cereal bowl with a straw attached and some other junk that I don’t need. If you must, make a plan or list and stick to your plan.

- Remember the big picture.